How you shop matters.

Shopping for health insurance can be... a pain! There are lots of forms, confusing fine print, and it's tough to tell if someone is trying to help you or sell you something. When we shop for phones, TVs, cars, or shoes we know how to be good consumers. However, when we shop for health insurance, research shows over 85% of people will choose the wrong health plan this year, costing them over $500 in unnecessary health expenses. Ouch!

This short guide is meant to empower you to make a smart health insurance decision. We'll share some tips and introduce you to our consumer-friendly online tool at TakeCommandHealth.com. We'll also demonstrate how it can help you save time and money!

Who we are: We're Take Command Health. Our mission is to make you a savvy health insurance consumer. We equip individuals with the tools and knowledge they need to make smart health insurance decisions. On average, our recommendations help our clients save over $500 a year.

5 tips to shop smart (and save money!)

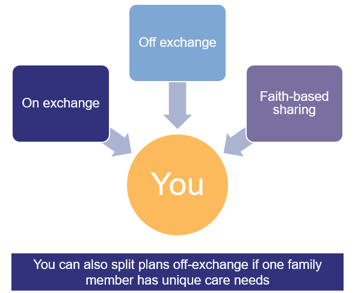

Tip #1: Know your options.

Most people aren't aware of how many options they have when shopping for health insurance. When you shop at Healthcare.gov, you're only seeing "on-exchange" plans. However, insurance companies only make a fraction of their plans available "on exchange". If you go directly to an insurance company's website, you'll see their "off-exchange" plans. There are also private exchanges, co-ops, and even faith-based "medical sharing" plans that function similar to insurance.

At TakeCommandHealth.com, we can help you quickly see ALL of your options. We have plans from all the major carriers that you'll find "on exchange", many of their "off-exchange" plans, and even faith-based plans like Medi-Share. When you shop for an airline ticket or a hotel, smart shoppers don't look at just one airline or hotel brand, they start on one of the awesome comparison sites like Kayak, Hotwire, Priceline, etc. where they can see everything. At TakeCommandHealth.com, we help you see more options!

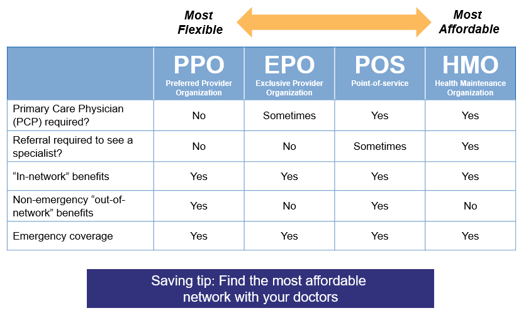

Tip #2: Know your doctor preferences.

In 2016, doctor networks are becoming more "narrow". This is insurance speak to say that staying "in-network" is going to be more important as insurance companies are going to pay less and less if you see an out-of-network provider (unless it's an emergency, of course). Most people know about PPOs and HMOs, but there are some other in-between options a savvy shopper should know about:

Being "flexible" with which doctors you see is a huge savings opportunity. If you don't have many preferred doctors, consider an HMO. These are not the HMOs of the past, you still get coverage for emergencies anywhere in the country and many companies offer referrals by phone or online.

If you have a lot of doctors you want to see or if you don't want to have to get a referral to see a specialist, consider an EPO. It'll be cheaper and EPOs more readily available in 2016 than PPOs are. If you are desperate for a PPO, you can read about your options here.

At TakeCommandHealth.com, we have a first-of-its-kind universal doctor search tool. Search for your doctors and we'll tell you which networks and plans he or she accepts. It'll make your life much easier and you'll likely find a less expensive network that still has your doctors!

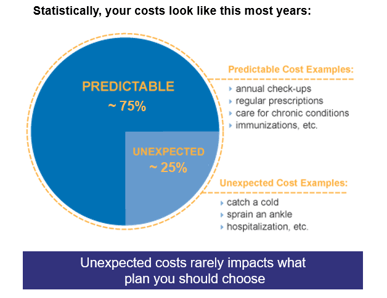

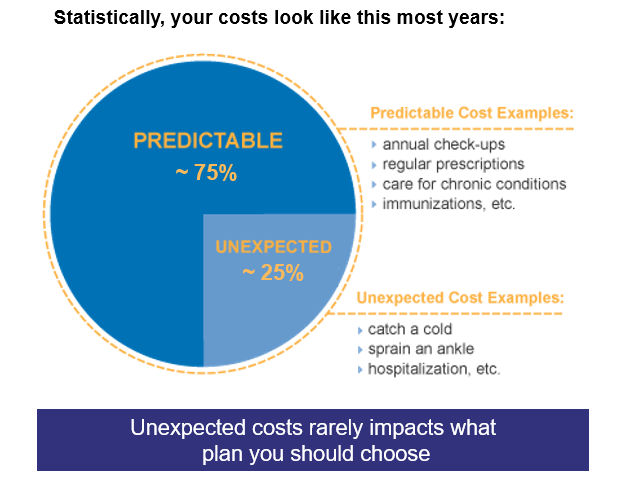

Tip #3: Estimate your out-of-pocket costs.

Yes, this is possible and it is critical to choosing the right plan! Statistically, over 75% of your costs in the next year are predictable based on your known needs:

We see people "over-buy" insurance because they are worried about catastrophic events such as accidents, serious illnesses, hospital stays, etc. The reality is most plans will cover those catastrophic events at roughly the same out of pocket cost to you. Don't believe us? The most you'll pay in a year is the out-of-pocket-limit for care plus your monthly premiums. A Bronze, Silver, Gold, and Platinum plan will be within a few hundred dollars of each other if you add it all up.

What really drives costs, and therefore your plan choice, are the things you know about: things like prescriptions, doctors visits, therapy, medical equipment, etc. If you're healthy, maybe you plan on none of these things--which is just as important to know too.

So which plan will cover your known needs the best and minimize your out-of-pocket expenses? At TakeCommandHealth.com, we've read all the fine print on deductibles, co-pays, and coinsurance for you. You can quickly search for your prescriptions or tell us about any health needs you are managing such as "physical therapy" or "having a baby." We'll run all the numbers for you and help you estimate your out-of-pocket costs on each plan! Brilliant!

Tip #4: Take advantage of tax credits, HSAs, etc!

One way to pay too much for health insurance is to leave money on the table. In Texas, we're particularly bad at this. Last year, at least 600,000 Texans could have claimed a tax credit but didn't. Part of the reason Texans left this money on the table is because going through Healthcare.gov can be challenging--so many people didn't know they were eligible!

At TakeCommandHealth.com, we'll help you quickly determine if you're eligible for tax credits and automatically apply them to your plan each month without the hassle of Healthcare.gov. Pretty awesome.

If you do make too much money for a credit, then you should probably consider using a Health Savings Account (HSA). HSAs allow you to pay for your care with tax-free dollars. For high-earners in a higher tax bracket, that's like a 30-35% discount on health costs! Our recommendation engine can help you determine if an HSA plan is a good fit for you.

Tip #5: Never never never buy dental insurance

Dental insurance is now almost completely separate from health insurance and it’s almost always a bad deal! Traditional dental insurance only works if someone (like a company) is helping you pay for it. Otherwise, if you take the time to read the fine print, you’ll realize that with waiting periods, maximum limits, and exclusions, it’s very very hard to get more out of your dental insurance than you put in. We compare it to an expensive layaway plan or pawn shop where they hold your money, charge you interest and fees, and then give you a little bit back when you visit the dentist.

What we really like and recommend are discount dental plans. Discount plans are not insurance--they are more like wholesale club memberships. You pay an annual fee and you get access to the same dentists and same rates as people who purchase traditional dental coverage. There are many discount dental plans and it’s easy to find one that your dentist works with. And get this: an annual membership costs the same as about 2 months of dental insurance.

Dental insurance is a great way to know if you’re being “sold” by a broker or website. They get HUGE commissions for selling dental insurance because it’s a money-maker for the insurance companies.

At TakeCommandHealth.com, we’ve set up partnerships with several discount dental providers. We can help you find your dentist and get you enrolled. (It's separate from your health insurance plan.) That advice alone will save you about $30/mo per person. You're welcome!

Let's do this!

If you've found this guide helpful, please share with your family and friends! We want everyone to learn how to get the most out of their health insurance. Reminder: the deadline for January 1st coverage is Dec 15th!

Ready to try out our tool? Visit TakeCommandHealth.com or click the link below!

{kind=link}